Introduction

Good morning. Thank you very much for the kind introduction.

I am very happy to participate in this conference on “Bank Regulation, Lending, and Growth,” sponsored by Columbia University and the Bank Policy Institute. The agenda covers a number of important banking issues and I will talk about the idea of policy efficiency from a supervisory perspective.1

Before beginning, let me emphasize that the views I express are my own and do not necessarily reflect those of the Federal Reserve Bank of New York or the Federal Reserve System.

Public policy strives to be efficient, but efficiency is not a simple concept, particularly in the context of the supervision of large financial firms where the world is complex, the official sector has multiple objectives, and impact lags are long and uncertain.2 For example, supervisors care about the safety and soundness of individual financial firms, about the provision of financial services to support the real economy, about consumer welfare and financial inclusion, and about financial stability. More generally, supervision and regulation are designed to both support productive financial intermediation and limit disruption and financial stability risks.3

Today, I will talk about a simple framework for one view of policy efficiency in a world of two policy objectives – financial intermediation and financial stability. As in traditional finance theory, one can think about an “efficient policy frontier” that maps the trade-offs among these objectives. One might choose a set of policies that supports a high level of financial intermediation and also accepts a higher risk of disruption or crisis. This might be achieved, for example, with relatively light oversight or low capital requirements. Alternatively, one might choose a different set of policies, such as more intensive oversight and stringent capital requirements that likely reduces risk, but also limits intermediation.

An efficient policy is one that minimizes risk for a desired level of intermediation—it is on the efficient policy frontier. This efficiency idea is distinct from the policy choice itself, as any of these policy regimes can be efficient in the sense that risk is as low as possible for a desired level of intermediation. I’ll emphasize that this framework is agnostic to the merits of one policy choice or another. That is, it is a positive framework and not a normative one, and I won’t look at this from a normative perspective. Policy preferences can vary and they are set by policymakers.

I believe this simple framework is useful when assessing and discussing changes to supervisory or regulatory policy that can be designed with different purposes in mind. For example, a policy change could be designed to increase efficiency and move toward the frontier. This could entail changing rules, regulations, or supervisory practices in order to promote more financial intermediation without increasing risk. Obvious examples could be eliminating a complex compliance regime for an activity that banks no longer perform or reducing redundancy in data reporting. It seems like a good idea to always pursue these types of efficiency gains.

Alternatively, a policy change could be designed to achieve a different risk and return profile. This could be a shift from a mix of policies designed to achieve a low-intermediation and low-risk outcome to a mix of policies designed to support higher intermediation while accepting greater risk. Either of these regimes can be efficient and consistent with policymakers’ preferences, but the expected outcomes would be quite different.

From a public policy perspective, in my view, it is important to be clear and distinguish between these two types of policy change. For example, one might expect a greater number of bank failures during stress if there were less effective supervisory oversight or higher borrowing costs in a world with higher capital requirements.4 Those may not be desired outcomes, but they would be predictable ones. From a risk management perspective, this might be viewed as an accepted risk of a particular policy choice. By contrast, a policy change designed to increase efficiency might not come with those undesirable outcomes.

In practice, however, it can be difficult to differentiate among drivers of policy change due to measurement and assessment challenges, the potentially long impact horizon, and different views from a social and private perspective. I’ll turn now to describe this efficiency framework and then discuss some of the practical issues.

Policy EfficiencyAs a point of departure, I’ll begin with an idea that I expect is familiar to most of you. Standard finance theory suggests that investors face a trade-off between risk and return that outlines the set of feasible options across portfolios. An investor can choose a portfolio with higher expected returns and higher risk, or a portfolio with lower expected returns and lower risk.

I think there is a useful analogy for supervisory and regulatory policy. On one hand, the official sector cares about the provision of financial services such as credit, deposit-taking, payments, and risk transfer, where effective intermediation supports economic growth and consumer well-being. This is the basic function of the financial sector and can be thought of as the return on banking. On the other hand, the official sector also cares about reducing disruption in the provision of those services and broader financial stability risks. It is only a decade since the financial crisis in 2008-2009 that imposed such an enormous social cost on the U.S. economy, so those risks remain salient for many of us.

In this context, the risk of disruption or a financial crisis matters because of the potential reduction of necessary financial services and economic activity in the future. As I discussed in a talk at this conference a few years ago, a short-term discussion of the balance between firm resilience and the provision of financial services may be reframed over a longer horizon as a dynamic trade-off between the provision of financial services today and in the future.5 This risk/return framework extends that perspective if one cares about the volatility of those financial services across different states of the world and over time.

The idea of multiple objectives suggests a policy trade-off with an efficient frontier. In this framework, an efficient financial sector regime can only realize more intermediation if it accepts a higher risk of financial instability and less intermediation in the future. A second premise is that the official sector can impact outcomes relative to this frontier through a combination of rules, regulation, and supervisory policies. For example, a reduction in loan documentation requirements, risk management reviews and supervisory oversight might allow increased lending in the short-run, but potentially lowers loan quality and increases risk over time.

A particular set and calibration of policies is efficient if the only way to increase financial intermediation is to accept higher risk of disruption or crisis. Equivalently, an efficient outcome is one where the only way to reduce risk is to accept less intermediation. This is not to say that all components of supervisory and regulatory policy come with this trade-off,6 but at some point, policy interventions become less effective, intermediation costs rise, and a trade-off is likely to emerge. Those points map the efficient policy frontier. The official sector can either push the financial sector along a given frontier as policy preferences change or closer to the frontier as policy becomes more efficient.

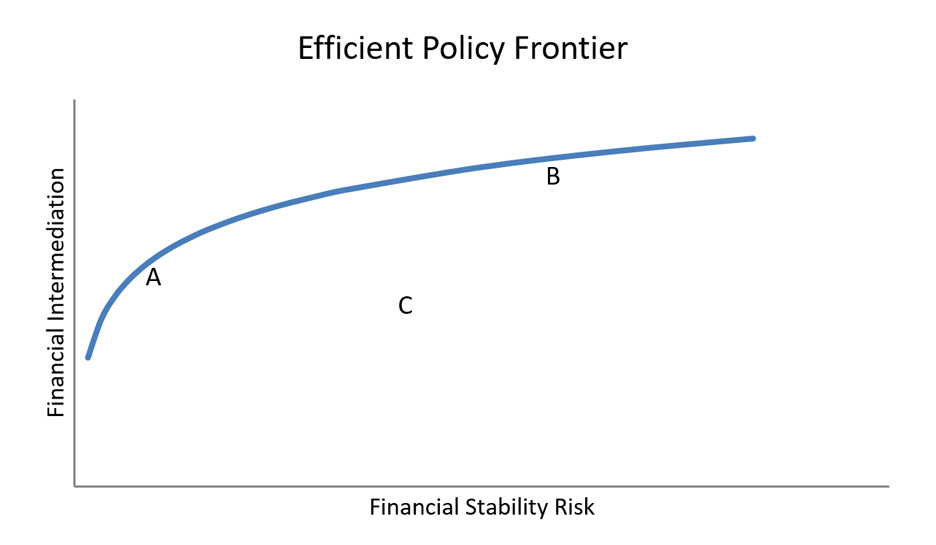

To be more concrete, consider the following chart with financial intermediation on the Y-axis and financial stability risk on the X-axis. Point A represents the outcome from a conservative policy mix with relatively low financial intermediation, but also relatively low financial stability risk. In this environment, supervisors might impose tight lending standards, so projects with positive net present value and low risk are potentially left unfunded. You might see high capital charges on relatively low-risk activities, restrictions or prohibitions on certain risky activities, or relatively frequent exams. Intermediation and credit growth might be slow on average, but more stable with less risk of a disruption to financial services or a financial crisis.

By contrast, point B represents the outcomes from a less conservative policy regime that supports more financial intermediation, but comes with a higher risk of disruption or financial crisis. In that environment, banks might be more inclined to assume a “risk-on” posture with looser underwriting standards, so riskier projects are funded. Oversight would be low and banks would feel less constrained. On average, greater intermediation would likely support more economic activity in the short-run but with a higher probability of disruption later on.7

Finally, point C represents an outcome from a policy regime that is not efficient. A different mix of policies could increase intermediation or decrease risk (or both) with no associated trade-offs. Point C is never a good outcome. Examples of such policies might be a burdensome compliance regime for activities that a bank doesn’t engage in, redundant data requests from the official sector, or a risk management system that does not address the most material risks.

To summarize, both point A and point B can be thought of as efficient outcomes, where the only way to support more financial intermediation is to accept higher risk. To be clear, one point on the efficient policy frontier is not necessarily better than another, and changes in policy to move between them reflect policymakers’ choices to promote social welfare. By contrast, point C is inefficient, and changes in the policy mix that push outcomes toward the efficient frontier are likely to be welfare-enhancing. The official sector should always be looking for opportunities to move the financial sector toward the frontier.

As a practical application of this framework, consider the Federal Reserve’s commitment to tailoring and ensuring that supervision is scaled appropriately to the risks associated with different types of institutions.8 Recent examples could include the stress testing distinction between large, complex firms and large non-complex firms; expanded eligibility for the 18-month exam cycle; relief from supervisory assessments, stress testing requirements, and other prudential measures for bank holding companies with less than $100 billion; the Bank Exams Tailored to Risk (BETR) program; and the multi-agency proposal to better align prudential standards with the risk profile of large institutions.9

Tailoring allows different firms to operate with different parameters of the policy regime. The largest, most systemically important firms, for example, impose larger potential risks to society than other firms, which implies a different risk/return trade-off and policy mix than for smaller institutions. Without the ability to tailor the regime to reflect the risks associated with different types of institutions, we would likely be left with a one-size-fits-all approach that is not optimal for any type of firm or for the financial system as a whole.

Discussion IssuesThe simple framework that I just described is just that—simple. The real world is much more complicated, and I’d like to spend a few minutes discussing some practical issues.

Understanding the Trade-offThe chart presented above is clearly illustrative and actual policy analysis requires detailed estimates of the potential benefits and costs of each component and the cumulative effect. For example, the Basel Committee published a framework to identify optimal levels of bank capital and used that framework as an input into the calibration of Basel III capital requirements.10 This approach considered how the probability of a financial crisis varies with bank capital, the social costs of banking crisis, the link between bank capital and bank funding costs, and the impact of higher loan spreads on economic activity.

Moreover, this efficient frontier is not fixed and is likely to vary over time as technology, official sector tools, and bank business models evolve. For example, technology-driven innovations that rely on bigger datasets and more sophisticated predictive algorithms might change the risk/return opportunities associated with certain intermediation services. Similarly, supervisory innovations like stress testing or more sophisticated horizontal assessments could make official sector oversight more effective. Finally, changes in business strategies like a shift to a more diversified business model might change the overall risk of certain activities. One can think of these changes as shifting the efficient policy frontier where there is more intermediation for a given level of risk. Alternatively, constraints on supervisory authorities or practices could shift the frontier in the opposite direction if use of effective tools is prohibited.

Given the complexity of these relationships, it is not surprising that there is a wide range of estimates and theories about the optimal type and level of oversight of financial institutions. Nonetheless, we need to understand better these relationships in order to make policy choices more effective. This is an area where I believe the official sector, industry participants, and researchers can all continue to make progress.

Social and Private PerspectiveA second interesting issue reflects the perspective on risk and return. In traditional portfolio investment problems, it is clearly the risk and return to the private investor. When thinking about policy, however, the appropriate perspective of the official sector is for society as a whole, which likely differs from the perspective of an individual firm. That is, the official sector and private sector might measure the axes differently—particularly the risk axis—because the official sector cares about spillovers, externalities, and other market failures that private actors may ignore.11

This broader perspective is a critical part of the supervisory framework for large banks that was implemented after the financial crisis. In particular, the official sector recognizes the potential impact that stress at a large bank could have on financial markets or the real economy. As a result, the Federal Reserve supervisory program pursues two complementary goals for large bank supervision—one, to enhance resilience to lower the probability of failure or inability to provide intermediation services and, two, to reduce the impact on the financial system or economy in the event failure or material weakness does in fact occur.12

This difference in perspective potentially introduces some divergence in views and assessment of what an efficient policy looks like. A set of policies might be socially efficient—that is, on the frontier when risk and return are measured for society as a whole – but perceived as inefficient by the industry or the public, who may focus on the private impact on individual firms or sectors. This can lead to some debate about the stated goals and assessment of the efficacy of a particular policy mix. I believe this is an area where better communication can help and the official sector can be clear on expected outcomes and explain any divergence between social and private perspectives.

Distinguishing Policy ChangesA third issue is that it is not always easy to distinguish policy changes that move outcomes along the frontier from policy changes that move outcomes toward the frontier. For example, is the shift to an 18-month exam cycle for community banks or a shift to less frequent stress testing for some banks an increase in policy efficiency or a shift to a different policy stance with different risk/return features? As I mentioned, both can be defensible policy moves, but they do have different implications. Moreover, a given policy change might have both effects as the stance of policy changes and the policy mix becomes more efficient. The proposal around the stressed capital buffer, for example, simplifies the capital regime and also relaxes some assumptions.13 Finally, these policy changes might interact and blend together.14

How do you know the policy intent? The most obvious answer is to look at the stated rationale and motivation associated with the policy change. For example, the analysis by the Basel Committee on the long-term economic impact of stronger capital and liquidity requirements accepted the potential costs of higher loan spreads and reduced output levels, so this can be viewed as movement to the left along a frontier.

It is also useful to think carefully about the expected impacts—both desired and undesired—and make ex ante predictions. What is the likely behavioral response? How might the balance sheet and the income statement change? What might financial markets reflect?

At the risk of taking this simple framework too far, let’s think about what might happen to market indicators in each of two scenarios—a movement toward the frontier that makes policy more efficient and movement along the frontier toward a less conservative policy stance. If the former is really an elimination of inefficient constraints (move from C to B, for example), one might expect equity prices and Sharpe ratios to rise, while CDS spreads or bonds ratings are flat as opportunities expand and risk doesn’t increase. By contrast, in a movement along the curve, say from A to B, one might expect equity prices to rise as intermediation opportunities increase, while CDS spreads and ratings deteriorate as risk increases. One might expect to see measures of increased distress in some states of the world over time.

Of course, the world is much more complex and risks materialize over long periods of time in response to many factors, and there are important differences between social and private outcomes, but I think it is helpful to think through these types of signals ex ante. By making predictions and assessing whether observed outcomes are consistent with those predictions, we can better understand the complex dynamics in financial institutions and develop better policy.

Resource EfficiencyFinally, I’ll emphasize that I have focused on one specific type of policy efficiency that looks at the ability to achieve multiple objectives. Alternatively, one could think about efficiency more directly in terms of resources and burden, both on the private sector and the official sector. For example, the Federal Reserve aims to minimize compliance burden while achieving its policy goals.15 That perspective is about allocative efficiency of scarce resources and the deadweight loss associated with the misallocation of those resources. As part of the official sector, we have an obligation to be good stewards of resources and should always try to achieve a given set of policy objectives in the least-cost manner.

ConclusionsTo conclude, I have suggested a simple framework to help distinguish changes in policy to achieve a different level of intermediation and an acceptable level of risk from changes in policy to increase efficiency. The first reflects the preferences of policymakers, and the second should be a standing goal. While it is difficult to make this distinction in practice, I believe it is useful to keep the difference in mind as we discuss and explain our work.

In my view, communication is vital, and we should explain our goals as clearly as possible and acknowledge all expected outcomes of policy changes. By recognizing the full set of expected outcomes, including those that are not desired, I believe we can more effectively communicate the goals of supervisory policy, increase accountability and transparency, and better fulfill our mission to promote a safe, sound and stable banking and financial system.

Thank you for your attention.