Introduction

I want to thank the Money Marketeers of New York University for inviting me to speak again today.1 These events provide a valuable forum for discussing the intersection of monetary policy implementation and money markets.

When I last spoke to this group in December 2020, there had been an historically rapid expansion of the Federal Reserve’s balance sheet associated with actions taken in response to the COVID-19 shock. These measures were highly effective at restoring market functioning and fostering accommodative financial conditions, helping the U.S. economy recover from the pandemic-related downturn. At the same time, they generated a significant increase in reserves supplied to the banking system. This year, even as the Federal Reserve’s balance sheet expanded at a more gradual overall pace, growth in Federal Reserve liabilities held by market participants—both in the form of bank reserves and in overnight reverse repo (ON RRP) facility balances—accelerated, and money market conditions shifted notably.

In my last talk, I suggested that one of the key advantages of the Federal Open Market Committee’s (FOMC’s) ample reserves operational framework is its flexibility, allowing monetary policy to be implemented efficiently and effectively across a range of environments. Today, I would like to share some observations on how the framework adapted to much higher levels of liquidity this year and is working as intended to support control over the federal funds rate and other short-term interest rates. I also want to highlight changes the FOMC has made in recent months to ensure the implementation framework continues to be effective through different environments, even on occasions when shocks disrupt markets.

Before I continue, let me note that the views I express today are my own, and do not necessarily reflect those of the Federal Reserve Bank of New York or the Federal Reserve System.

Recent Shifts In Liquidity Have Been Historically Large, And Money Market Rates Declined…

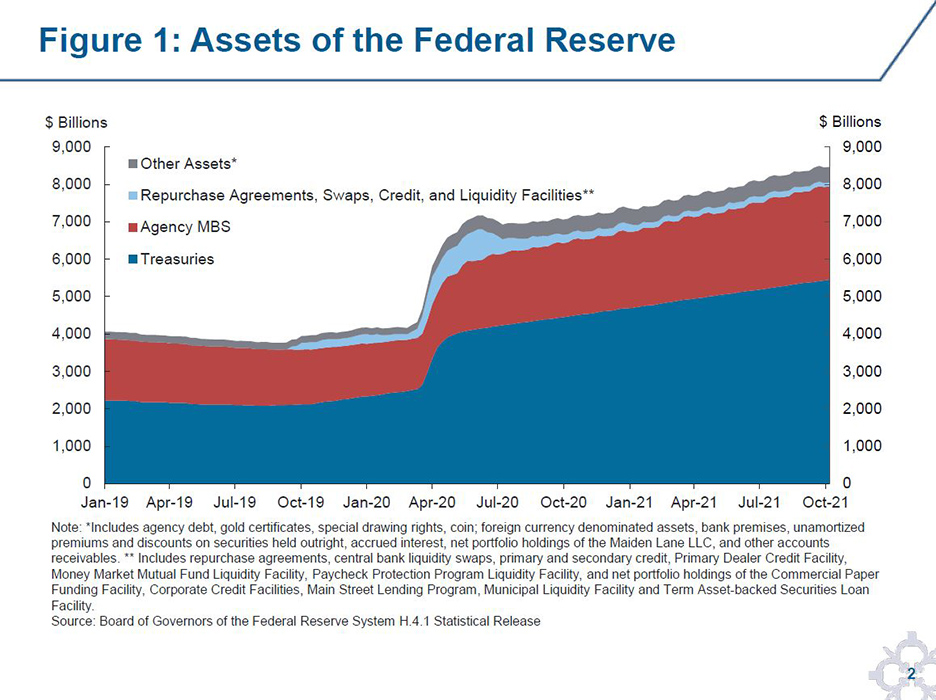

Let me start with a brief review of the recent evolution of the Federal Reserve’s balance sheet, and how this has influenced conditions in money markets. In response to the COVID-19 shock, the Federal Reserve, along with many other central banks, expanded its balance sheet to support the smooth functioning of financial markets, and maintain the vital flow of credit to households and businesses. From March to December 2020, the Federal Reserve’s assets increased by roughly $3 trillion, as shown in Figure 1.

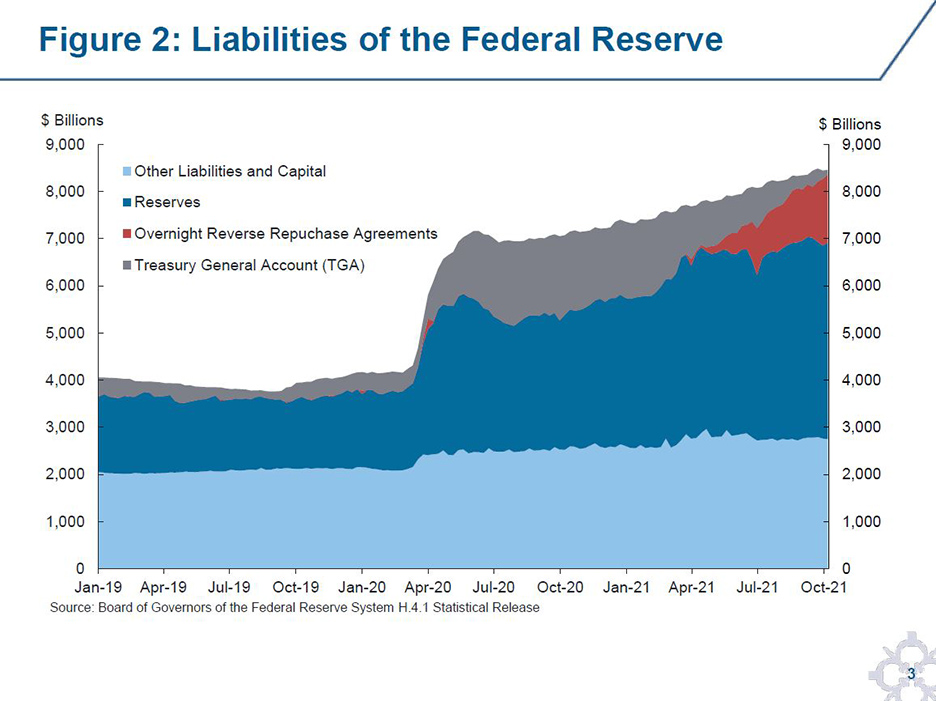

This expansion in assets could have been accompanied by a commensurate increase in Federal Reserve liabilities in the form of bank reserves.2 However, concurrent with the growth in the balance sheet in 2020, the U.S. Treasury’s General Account (TGA)—effectively Treasury’s cash account at the Federal Reserve—rose dramatically. Treasury increased the TGA to ensure sufficient cash was available to support programs aimed at helping American households and businesses weather the pandemic.3 Growth in the TGA, as indicated in Figure 2, limited reserve growth associated with the balance sheet expansion.

Starting in mid-2020, the pace of net asset purchases slowed, and in December 2020 the FOMC adopted guidance that it would continue to increase its holdings of Treasury securities and agency mortgage-backed securities (MBS) by at least $120 billion per month until substantial further progress had been made toward its economic goals.4 However, even with this more steady pace of balance sheet growth, Federal Reserve liabilities held by market participants—in the form of reserves and ON RRP balances—increased sharply in 2021, as indicated on the right in Figure 2. This resulted from the dramatic $1.5 trillion decline in the TGA since the beginning of the year.5

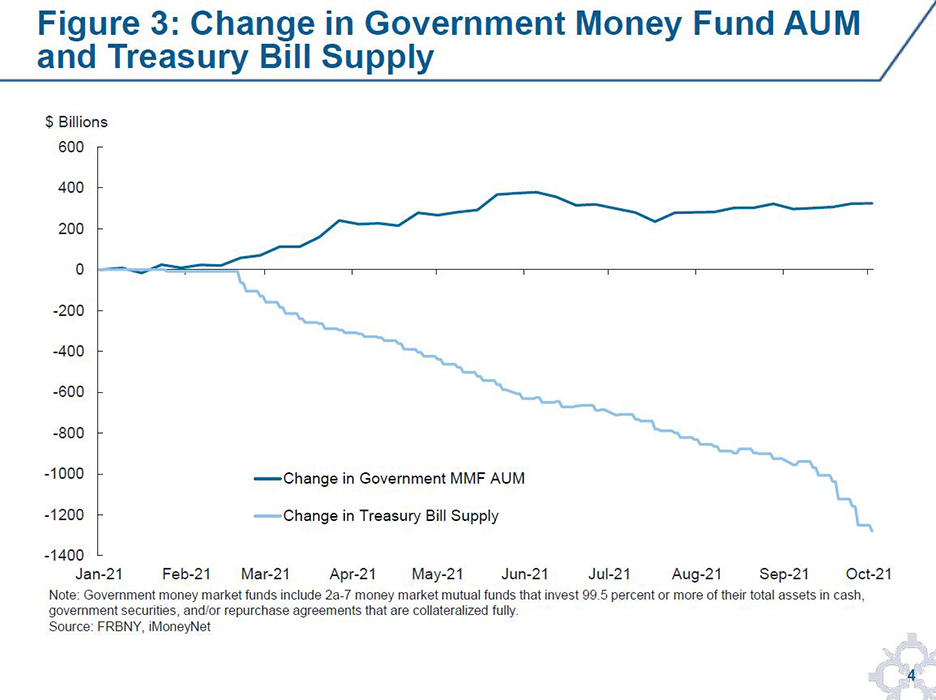

Unsurprisingly, the increase in reserves resulted in downward pressure on overnight interest rates—including the federal funds rate—relative to the interest on reserve balances (IORB) rate.6 As reserve balances rose, some banks perceived a cost to expanding their balance sheets further and lowered their deposit rates.7 In response, depositors and other investors shifted assets to money market mutual funds (money funds), which raised demand for money market investments and put downward pressure on money market rates more broadly. On the year, government money fund assets under management (AUM) have increased by over $320 billion, as shown in Figure 3.

It’s important to note that at the same time demand for money market investments rose, the net supply of U.S. Treasury bills—an essential investment for money funds and other investors—fell by an historically large amount: over $1.2 trillion so far in 2021, as indicated in Figure 3. This combination of increased liquidity and reduced supply of investment options had the potential to put substantial further downward pressure on overnight rates, including the federal funds rate.

…The ON RRP Facility Worked As Intended To Support Rate Control

The ON RRP facility was established as part of the FOMC’s ample reserves framework in order to support interest rate control in a wide variety of environments. It offers a broad range of money market investors the option to invest in an overnight reverse repo with the Federal Reserve, which improves their bargaining power for private investments. It also offers an alternative investment when private investments are not available at rates above the ON RRP rate.8

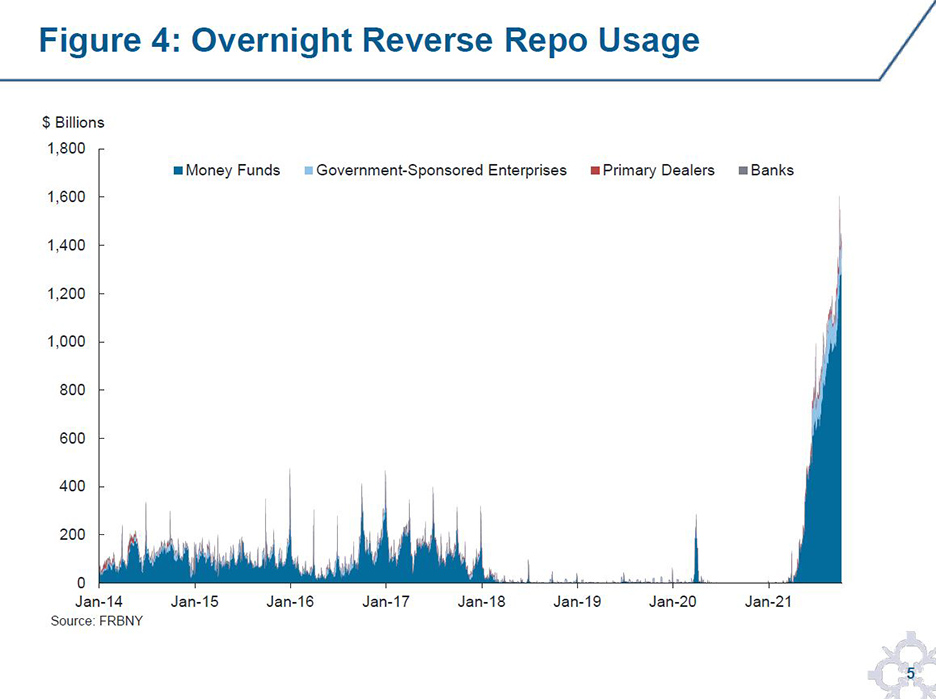

In the first quarter of this year, ON RRP facility usage became more regular, and it has increased rapidly since. Recently, reductions in the TGA and Treasury bill supply have accelerated, and the ON RRP facility has exceeded $1.2 trillion consistently since mid-September, as shown in Figure 4.

The ON RRP facility is working as intended, even as usage expands to new highs. Just as IORB creates a floor for rates on bank lending activity, the ON RRP facility supports control of the federal funds rate by providing a soft floor for the overnight money market activity of a broader set of money market participants.9 Usage of the facility also broadens the holders of Federal Reserve liabilities beyond banks, easing pressure on bank balance sheets that may result from reserve growth. As shown in Figure 2, the supply of reserves has increased relatively modestly this year, as the ON RRP facility absorbed much of the increase in liquidity from the decline in the TGA and ongoing asset purchases.

An essential feature of the ON RRP facility is that it has a fixed rate and therefore its size is determined by the interest rate environment.10 Just as usage of the facility grew in response to downward pressure on money market rates, it should decline in response to increases in them. For example, if Treasury were to expand Treasury bill supply and interest rates on these instruments rose above the ON RRP rate, investors should naturally reallocate out of the facility and back into these assets. Similarly, if the supply of reserves declines and rates rise relative to the IORB rate, ON RRP balances should naturally recede. This dynamic has been observed in the past. Following the expansion of the Federal Reserve’s balance sheet in response to the Global Financial Crisis, the level of reserves began to decline in 2014, and as money market rates moved away from the ON RRP rate, usage of the facility gradually fell back to zero.

The flexible size of the ON RRP facility helps the FOMC’s ample reserves framework adapt smoothly to different reserve and money market environments. The FOMC has indicated that, with the federal funds rate likely to be constrained by its effective lower bound more frequently than in the past, it is prepared to use its full range of tools—including large-scale asset purchases—to achieve its maximum employment and price stability goals.11 As such, extended periods of elevated ON RRP usage may be a relatively regular feature of the ample reserves framework. This isn’t a challenge for monetary policy implementation; it’s the framework working as designed.

Modest Adjustments Were Made To Terms Of Implementation Tools To Evolve With The New Environment…

Even with the ON RRP facility promoting interest rate control this year, the Federal Reserve has made some modest adjustments to its implementation tools.

As I’ve just described, IORB provides a floor for bank lending rates, and the ON RRP facility supports control of the federal funds rate by creating a floor beneath the overnight activity of a broader set of money market participants. Earlier this year, the IORB rate was 10 basis points and the ON RRP rate was zero. Unsurprisingly, as reserves increased, the effective federal funds rate (EFFR) edged further below the IORB rate and closer to the bottom of the FOMC’s target range. Against the backdrop of declining Treasury bill supply and rising government money fund AUM, overnight secured rates fell to near zero.

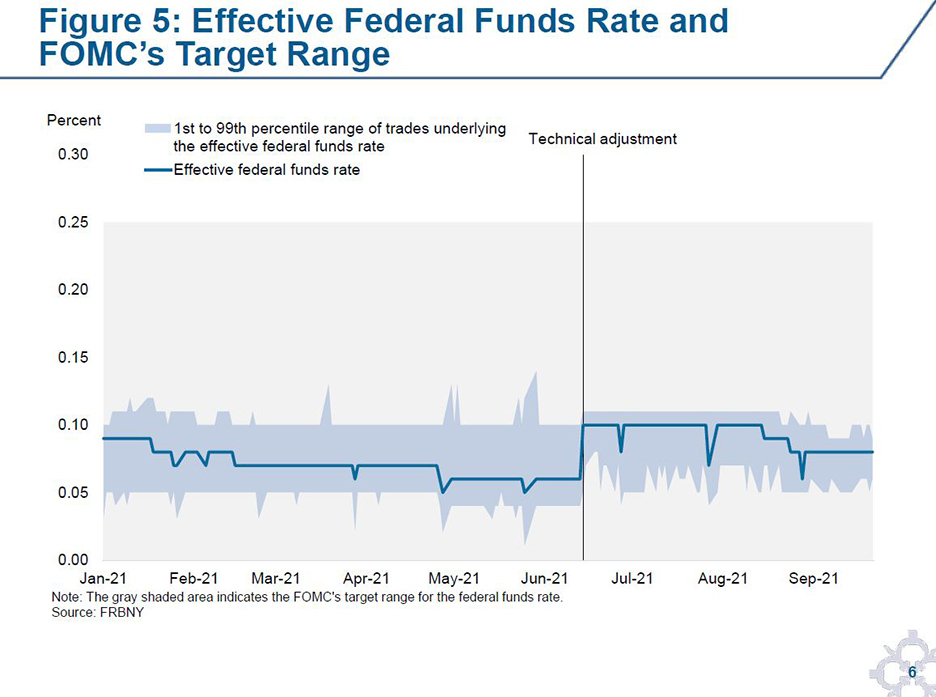

The Federal Reserve implemented a technical adjustment to administered rates in June, lifting the IORB and ON RRP rates by five basis points each, shifting up their position in the target range. This was a normal adjustment in response to evolving money market conditions, intended to help maintain the federal funds rate well within the target range. Lifting the ON RRP rate above zero also helped support the smooth functioning of money markets. With secured rates near zero, money funds with stable net asset values (NAVs) could have experienced challenges covering operating costs and limited inflows, increasing the potential for further downward pressure on rates.

This was the sixth such technical adjustment. Like the five adjustments before, it worked as expected. Both secured and unsecured overnight rates shifted modestly higher, in line with the change in the two administered rates. As shown in Figure 5, throughout this year not only has the EFFR printed well within the target range, but the bulk of trading in the federal funds market—as shown by the 1st and 99th percentiles of trades underlying the EFFR—has also fallen within the range.

The adjustments to the Federal Reserve’s policy implementation tools this year haven’t been limited to administered rates. To ensure the ON RRP facility is effective, it is important to provide access to a sufficiently broad set of money market participants and to offer counterparties adequate investment capacity.

In April, the eligibility requirements for RRP counterparties were adjusted to make the facility more accessible, in line with the New York Fed’s efforts to ensure that its counterparty policies both support effective policy implementation and promote a fair and competitive marketplace. Since then, we have onboarded new RRP counterparties, increasing the diversity of our counterparty base.

The ON RRP facility’s per-counterparty limit has also been adjusted this year. In March, the FOMC lifted the limit to $80 billion to account for changes in the size and concentration of the money fund industry since 2014, and to ensure sufficient capacity to maintain an effective floor under the federal funds rate. Most recently, as ON RRP usage steadily increased, the FOMC raised the limit again, this time to $160 billion. Since the increase, some counterparties have participated in ON RRP operations for more than $80 billion, including on the September quarter-end date.

…And Additional Tools Were Added To Strengthen The Policy Implementation Framework

In order for the FOMC’s ample reserves framework to effectively support policy implementation through different environments, it also needs to be resilient to occasional shocks that can arise. In recent years, we have observed that pressures in money markets can emerge rapidly, and that these can spill back into the federal funds market. Based on the effectiveness of repo operations to support policy implementation, particularly during periods of stress, the FOMC established two new standing overnight repo facilities at its July meeting: a domestic standing repo facility, the SRF, and a repo facility for foreign and international monetary authorities, the FIMA Repo Facility.12

The SRF is intended to address pressures in the repo market that can spill into the federal funds market, and to flexibly add reserves, when needed. Both primary dealers and banks can access repo funding through the SRF against a limited set of high-quality securities: U.S. Treasuries, agency debt, and agency MBS.13 While primary dealers have long been counterparties to the Federal Reserve’s open market operations, the FOMC decided in July to add banks as eligible counterparties to the SRF, which allows them to access the facility on similar terms as primary dealers. Additionally, banks are key participants in the federal funds market and adding them should enhance interest rate control by offering a backstop source of liquidity. Earlier this month, the New York Fed began accepting formal expressions of interest from banks to become SRF counterparties. Several have started the process, and we expect the first group of banks will be able to participate in the SRF early next year. I encourage banks interested in learning more about the SRF to reach out to the New York Fed.14

The FIMA Repo Facility is available to help address global dollar funding pressures that can emerge. Disruptions in global funding markets have the potential to negatively impact financial conditions faced by U.S. households and businesses, in particular during significant stress events in broader financial markets. The FIMA Repo Facility provides foreign official accounts a source of temporary liquidity against their holdings of Treasury securities at the New York Fed to address these pressures. Foreign account holders have responded positively to the establishment of the facility, as it provides an alternative to outright sales and complements the existing U.S. dollar liquidity swap lines by extending access to dollar funding to a broader range of foreign official institutions.

Importantly, in the FOMC’s ample reserves framework, the role of the ON RRP facility and the new repo facilities are not symmetric. These new repo facilities, while offered daily, are not expected to be used regularly. The FOMC is committed to maintaining an ample supply of reserves to ensure that administered rates—the IORB and ON RRP rates—exercise control over the federal funds rate. So, whereas the ON RRP facility could see persistent usage in some environments, these new repo facilities are only intended to act as occasional backstops.

Looking Ahead, Working To Ensure Implementation Framework Remains Flexible And Adaptable…

I’ve talked today about how the Federal Reserve’s ample reserves framework has ensured effective policy implementation recently by adapting to evolving money market conditions, and about some of the new tools added to the framework. However, market structure continuously evolves, which in turn can have important implications for the framework. Recognizing that, I would like to share a few thoughts on two important changes on the horizon.

The first is work to improve the resilience of the U.S. Treasury market. In light of the disruptions in March 2020, and also shorter-lived disruptions on other occasions, market participants, academics, and the official sector have been analyzing underlying vulnerabilities in the Treasury market. While the new standing repo facilities are designed to support effective policy implementation, I expect they will also contribute to smooth functioning of the Treasury market by ensuring temporary liquidity is available against Treasury securities. More broadly, the Inter-Agency Working Group for Treasury Market Surveillance (IAWG), of which the New York Fed and the Federal Reserve Board are members, has identified several key areas for further study to improve Treasury market resilience.15 Some of this work could result in important changes to market structure that are relevant for the FOMC’s implementation framework. For example, on the Open Market Trading Desk at the New York Fed (the Desk), we have been attentive to developments around expanded central clearing. These could ultimately merit a study of the costs and benefits of central clearing for some of the Desk’s open market operations to ensure their ongoing effectiveness.16

Looking further ahead, a second area that could have material implications for policy implementation is technological innovation in payments and money. Around the world, financial market participants and the public are seeking faster and cheaper payment settlement. This desire is resulting in the development of new, private-sector means of transfer, such as stablecoins, and the study of public-sector solutions, like central bank digital currencies (CBDC) and faster payments.17 The Federal Reserve itself is undertaking an initiative called FedNow that will enable banks to provide safe and efficient instant payment services. And, the Federal Reserve Board will soon be publishing a paper to engage the public on policy issues associated with a U.S. CBDC. On the Desk, we are focused on the broad implications of financial innovation for monetary policy implementation. While it’s not yet clear how the money and payment ecosystem will evolve in the future, it seems apparent that there will be important implications for markets and policy implementation. But I want to return to the theme I started with: the implementation framework is flexible, and it will be adapted as needed to implement monetary policy efficiently and effectively.

Transitioning Away From LIBOR, Only 79 Days Left

As I wrap up my remarks, I would be remiss if I didn’t mention a fast-approaching, critical milestone in the transition away from LIBOR. After a yearslong effort to reduce the financial stability risk posed by the use of this flawed reference rate, this year will effectively mark LIBOR’s end. While U.S. dollar LIBOR will continue for a little while in order to support the transition of legacy contracts, supervisory guidance has been clear that banks should stop entering into new U.S. dollar LIBOR-linked contracts no later than the end of this year.18,19

The New York Fed plays an important role in supporting a smooth transition away from LIBOR. Jointly with the Federal Reserve Board, we convened the Alternative Reference Rates Committee (ARRC), and we produce the Secured Overnight Financing Rate (SOFR). We also operate in financial markets, and need to transition ourselves. To prepare for the end-of-year deadline, we reviewed our contracts with our trading counterparties and are amending these contracts to replace existing U.S. dollar LIBOR references with ones linked to SOFR. These documents should be fully executed by the end of October.

While there has been significant progress in the overall transition to date, there is still more work that must be done. Not only is it imperative that firms around the world act without delay, it’s equally important that they are prudent in their choice of alternative reference rates. The official sector has repeatedly emphasized the importance of using alternatives that can be reasonably expected to remain robust and resilient.

The ARRC selected SOFR as its preferred alternative to U.S. dollar LIBOR for institutions of all sizes because it is based on a market that is vast and liquid, with nearly $1 trillion of daily transactions by a diverse set of borrowers and lenders underlying the rate. SOFR isn’t the only alternative available, but it certainly is the most robust, most liquid option. If market participants opt to use rates other than SOFR, they should make sure they fully understand how those rates are constructed and any fragilities associated with them.20

Thank you for your attention, and I would like to again thank the Money Marketeers for the opportunity to speak with you today. I look forward to the discussion with Dov.