-

-

The Teller Window is a publication featuring expert knowledge and insight from the New York Fed, including thoughts and perspectives from senior leaders.

Do you have a request for information and records? Learn how to submit it.

Learn about the history of the New York Fed and central banking in the United States through articles, speeches, photos and video.

-

-

-

The Governance & Culture Reform hub is designed to foster discussion about corporate governance and the reform of culture and behavior in the financial services industry.

Need to file a report with the New York Fed? Here are all of the forms, instructions and other information related to regulatory and statistical reporting in one spot.

The New York Fed works to protect consumers as well as provides information and resources on how to avoid and report specific scams.

-

-

-

The New York Innovation Center bridges the worlds of finance, technology, and innovation and generates insights into high-value central bank-related opportunities.

The growing role of nonbank financial institutions, or NBFIs, in U.S. financial markets is a transformational trend with implications for monetary policy and financial stability.

The New York Fed offers the Central Banking Seminar and several specialized courses for central bankers and financial supervisors.

-

-

| This new series, produced by the Research Group's Publications Function, focuses on the academic and public policy issues shaping our research. |

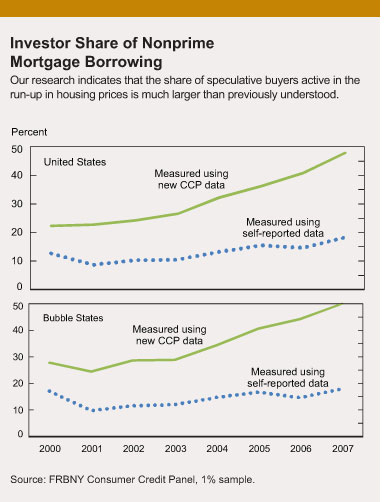

| The Dynamics of Housing Prices New York Fed economists are among those seeking to understand the steep rise and decline in housing prices at the root of the 2007-09 financial crisis. A recent study in our Staff Reports series, “Real Estate Investors, the Leverage Cycle, and the Housing Market Crisis,” investigates the role of speculative buyers, arguing they were present in the housing market in larger numbers than previously understood and behaving in ways that exacerbated both the boom and bust in home values. Tapping a relatively new data source, the FRBNY Consumer Credit Panel (CCP), the New York Fed authors say they are able to improve on estimates of the share of so-called buy-and-flip investors active in the bubble market. By their count, the share of new U.S. mortgage borrowing going to investors buying multiple homes grew from around 20 percent in 2000 to nearly 35 percent at the peak of the market in 2006. In states with the most pronounced housing cycles—the “bubble states” of Arizona, California, Florida, and Nevada—the investor share increased faster, rising from almost 25percent in 2000 to 45percent six years later.  The authors also observe that the share of borrowers in the “crucial” nonprime sector who were acknowledging their investor status on their mortgage applications was relatively low and constant—less than 20 percent throughout the boom. Yet by incorporating fuller credit-report information available with the CCP, the authors could “see through” the data that was self-reported by borrowers and thus determine that the investor share at the peak of the housing market was more than double the recognized rate (see chart.) The authors also observe that the share of borrowers in the “crucial” nonprime sector who were acknowledging their investor status on their mortgage applications was relatively low and constant—less than 20 percent throughout the boom. Yet by incorporating fuller credit-report information available with the CCP, the authors could “see through” the data that was self-reported by borrowers and thus determine that the investor share at the peak of the housing market was more than double the recognized rate (see chart.)The analysis helped the researchers demonstrate that the investor group had a more bullish view of the market than other homebuyers; for example, investors were taking advantage of weakening credit standards to put less money down and gravitating toward nonprime credit, even if more expensive, to make purchases. Some scholars of bubbles argue that such “optimistic” buyers, using leverage to make increasingly large bets on the direction of prices, drive an asset-price boom. Their propensity to default, if expectations aren't realized, subsequently contributes to the intensity of a decline. The authors—Andrew Haughwout, Donghoon Lee, Joseph Tracy, and Wilbert van der Klaauw—say their paper provides the first direct evidence of a “leverage cycle” at work in the housing market. They add that understanding how the housing bubble fits this pattern points to potential policy solutions, such as restrictions on the use of leverage. Haughwout says the researchers still have further work to do on the question of whether buy-and-flip investors generated price amplification, or simply responded to it. A next step would be to show convincingly that it was a loosening of credit standards that allowed investors to take a more active role and to drive prices up. If you get that causality right, he explains, then clear policy prescriptions follow. Further Reading: Andrea Ferrero investigates the connection between soaring house prices and current account deficits: “House Price Booms, Current Account Deficits, and Low Interest Rates” Check out the first paper to test the asset pricing implication of leverage in a laboratory: “Leverage and Asset Prices: An Experiment” Read research considering explanations for the rise in early defaults on nonprime mortgages from 2001 to 2007: “Juvenile Delinquent Mortgages: Bad Credit or Bad Economy?” |

||||

|