It is a pleasure to join you virtually today. I’m grateful to SIFMA for the kind invitation to discuss the Federal Reserve’s ongoing asset purchases and to all of you here today for your interest in the smooth functioning of financial markets.1

In response to the severe economic shock associated with the Covid-19 pandemic, the Federal Reserve is committed to using all of its tools to achieve its goals of maximum employment and price stability. The Federal Open Market Committee (FOMC) has cut the target range for the federal funds rate close to zero. Additionally, the Fed has taken a wide range of steps—many in coordination with the U.S. Treasury—to support the flow of credit to households, businesses, and state and local governments. These steps have targeted many different parts of the financial system and economy. Liquidity tools are supporting funding markets. Credit facilities are helping to ensure that small businesses, corporations, and state and local governments have access to credit. And, regulations have been temporarily adjusted to encourage bank lending. Another important measure, and the focus of my talk today, is the asset purchases that we have conducted at an unprecedented scale and speed to support the smooth functioning of markets for Treasury and agency mortgage-backed securities (MBS)—both of which play crucial roles in the American financial system and economy.

In early to mid-March, amid extreme volatility across the financial system, the functioning of Treasury and agency MBS markets became severely impaired. Given the importance of these markets, continued dysfunction would have led to an even deeper and broader seizing up of credit markets and ultimately worsened the financial hardships that many Americans have been experiencing as a result of the pandemic.2 The FOMC responded quickly and decisively with substantial purchases of Treasury securities and agency MBS, and then demonstrated an even more forceful commitment to market functioning by directing the Open Market Trading Desk (the Desk) to make purchases “in the amounts needed to support the smooth functioning of markets” for those securities.3

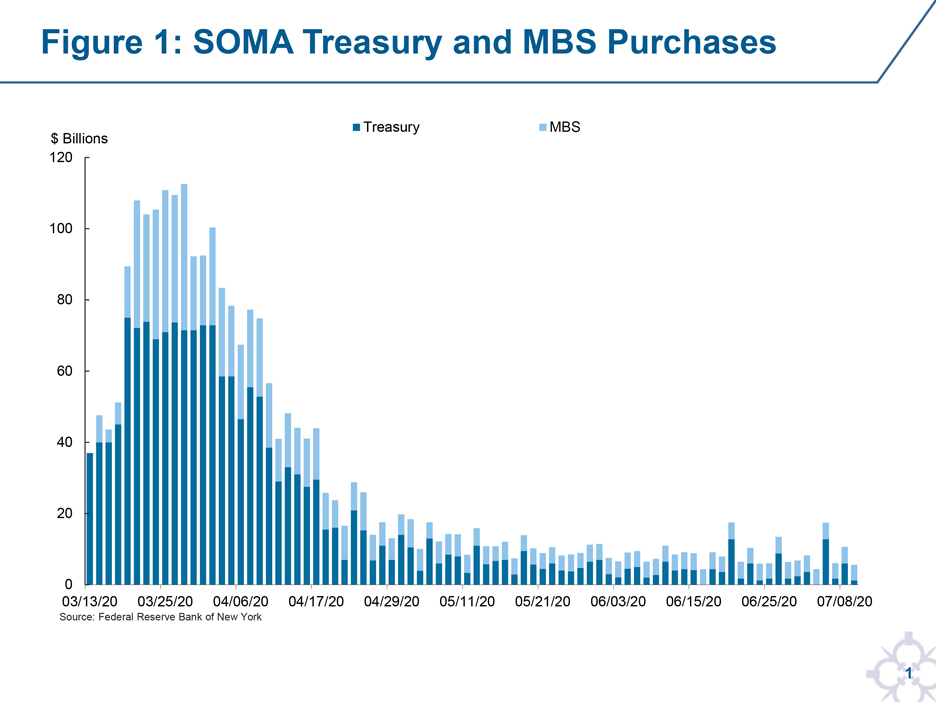

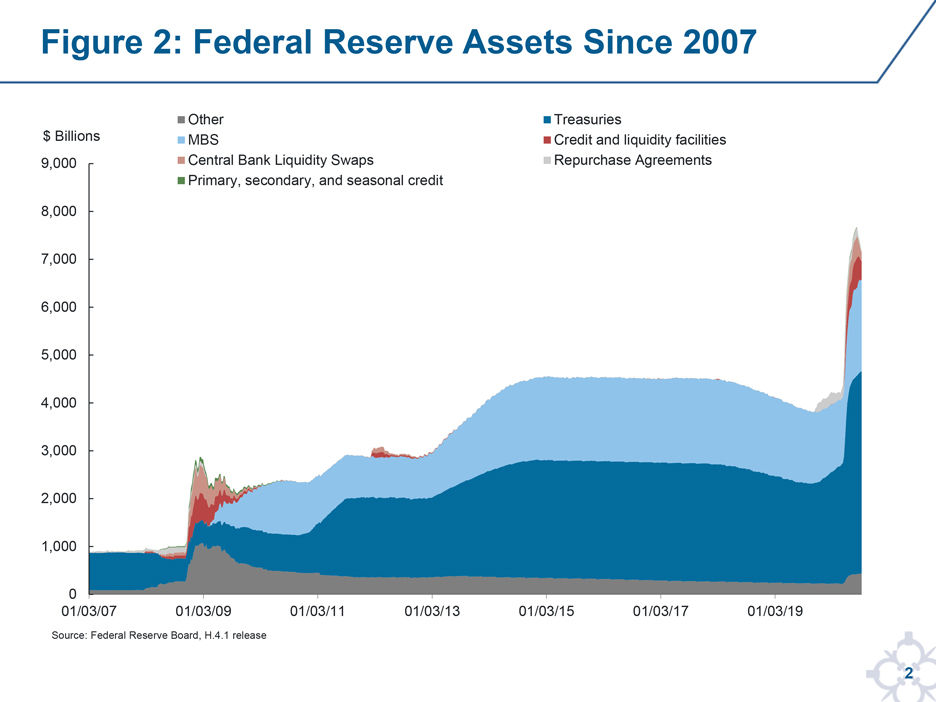

Asset purchases are a standard tool of monetary policy implementation. Traditionally, the Desk has used Treasury purchases to maintain the supply of reserves in accordance with the FOMC’s policy implementation regime. Following the Global Financial Crisis, the FOMC used asset purchases primarily to exert downward pressure on longer-term interest rates, or in the case of MBS to ease mortgage rates, when the federal funds rate was at its effective lower bound. The purchases during this most recent episode have been distinct in both their purpose, to address disruptions in market functioning, and their scale and speed, which have been unparalleled. As shown in Figure 1, System Open Market Account (SOMA) securities holdings grew at an extraordinary pace, with purchases totaling more than $100 billion on some days. Cumulatively, the purchases since mid-March have totaled $1.7 trillion of Treasuries and more than $800 billion of agency MBS,4 which represents the vast majority of the overall $2.6 trillion increase in the Federal Reserve’s balance sheet since then, as shown in Figure 2.

To assess the pace of purchases needed to support market functioning, we used extensive metrics along with our best judgment. The initial rapid pace of purchases was motivated by a severe breakdown in the functioning of these markets. As market functioning improved, we substantially slowed our pace of purchases. Most recently, at its June meeting, the FOMC decided to increase holdings of Treasuries and agency MBS “at least at the current pace to sustain smooth market functioning.”

Today, I’d like to talk about the disruption we saw and the steps we took in response. I will focus on three broad questions. First, what is smooth market functioning and why does it matter? Second, how have our asset purchases supported smooth market functioning? And third, how will we structure purchases to sustain market functioning over coming months and remain vigilant against renewed deterioration? Let me note that the views I express are my own and do not necessarily reflect those of the Federal Reserve Bank of New York or the Federal Reserve System.

What Is Smooth Market Functioning, and Why Does it Matter?

Before I describe our response to the recent crisis, I want to share how we think about smooth functioning in Treasury and agency MBS markets, and why it is so critical to the U.S. economy. I’ll focus on what we perceive as two important characteristics of smoothly functioning markets: liquidity and efficient pricing.5

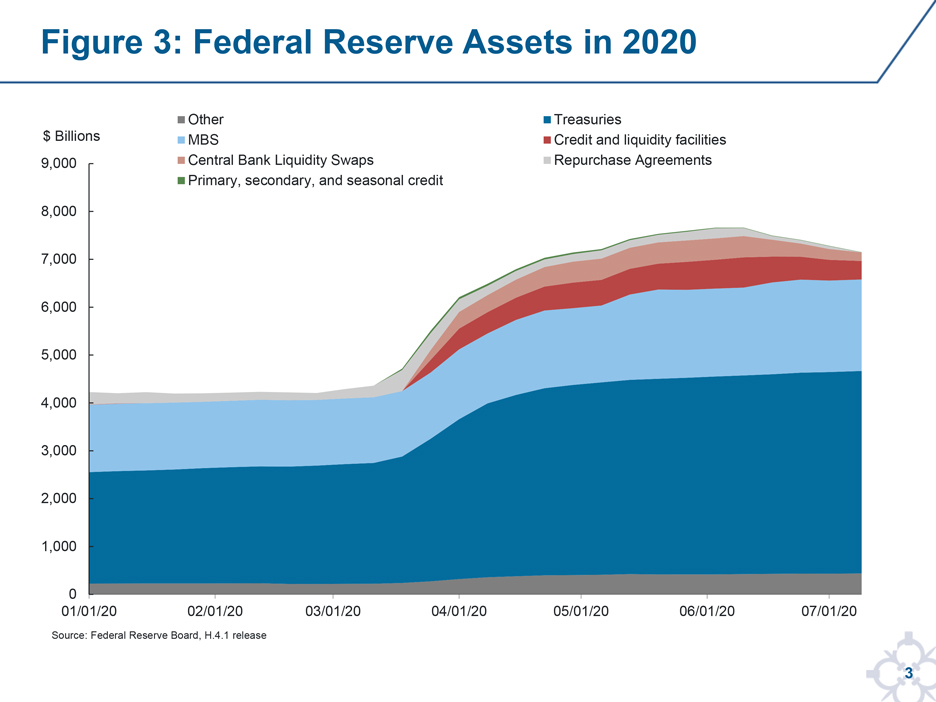

Liquidity comes in many forms. One form of liquidity is the availability of financing for existing or new positions. I think of this as funding liquidity. Another form of liquidity is the ease with which assets can be bought and sold, often called market liquidity. Although these concepts are distinct, they are related and reinforcing.6 When funding liquidity is abundant, market participants can finance the transactions that produce market liquidity. My comments today focus on how we have used asset purchases to support market liquidity, but I do want to note that the steps the Federal Reserve took at the same time to support funding markets almost certainly contributed to market liquidity. In fact, funding markets are now functioning quite well. As a result, as you can see in Figure 3, which is a close-up of my previous chart, our repo book has rolled off over recent months and is now down to zero, and usage of most other funding programs has also diminished.

Liquid markets allow participants to transact quickly and at low cost, so they can easily adjust their positions in response to their own changing circumstances or broader economic developments. In normal conditions, the markets for Treasury securities and MBS are highly liquid. Confidence in the liquidity of Treasuries persuades investors to accept lower yields on these securities,7 and because Treasury interest rates are a benchmark for many other rates, these lower yields ultimately reduce borrowing costs for families, businesses, and state and local governments. Similarly, the liquidity of agency MBS helps investors to transact quickly and efficiently in residential mortgage loans, which results in lower mortgage interest rates for households. Supporting the liquidity of these markets has been an important component of the Federal Reserve’s actions to bolster the flow of credit and the effective transmission of monetary policy during the pandemic.

Turning to efficient pricing, one can always debate whether any given asset price is right. However, we generally expect prices of instruments with identical or very similar cash flows to be closely connected, so opportunities for arbitrage are limited, and relative value spreads are small. In smoothly functioning markets, if prices of related instruments diverge, arbitrageurs sell the securities with high prices and buy those with low prices, profiting from the difference and pushing the prices back together. When arbitrage breaks down, the resulting mispricings make financial markets less useful for risk management and investment, which can ultimately restrict the flow of capital in the economy.

In practice, market liquidity is never perfect, and pricing discrepancies are never entirely eliminated. Liquidity providers—who buy securities from clients who wish to sell, and then look for other clients who wish to buy—are compensated for this service in the form of bid-ask spreads or other transaction costs. Likewise, investors do not exploit all arbitrage opportunities, because arbitrage typically requires capital and funding and entails transaction costs, as well as the risk of loss if the price difference widens rather than narrows. As a result, prices of closely related securities can sometimes diverge. Still, when the Treasury and agency MBS markets are functioning smoothly, transaction costs and price divergences should typically be small.

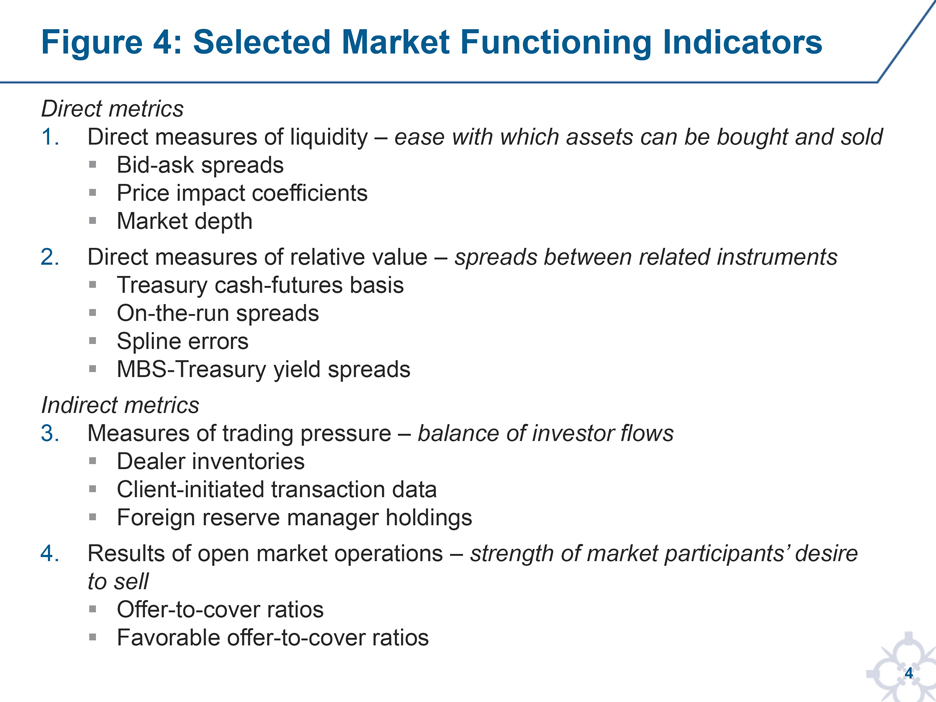

Markets are complex. No one indicator can show whether a given market is functioning smoothly. On the Desk, we use a suite of complementary categories of indicators to assess the functioning of Treasury and agency MBS markets. Without diving too deeply into these indicators, I’ve summarized the categories in Figure 4. The first category includes direct measures of liquidity, such as bid-ask spreads, price impact coefficients and market depth.8 The second category includes direct measures of relative value, such as the Treasury cash-futures basis, on-the-run spreads, spline errors, and MBS-Treasury yield spreads. The remaining categories contain indirect metrics. Instead of showing how well markets are functioning, these metrics reveal forces that can lead to breakdowns of liquidity and efficient pricing. In particular, we look at measures of trading pressure, which can show whether there is an imbalance between the volume of sales and the volume of purchases, and at the results of our open market operations, which can provide signals about the intensity of market participants’ desire to sell securities as well as other market conditions.

How Have the Federal Reserve’s Asset Purchases Supported Smooth Market Functioning?

The extreme shock to the economy and financial markets as the pandemic spread in early March led to a swift and severe deterioration in the functioning of the Treasury and MBS markets. Pessimism and uncertainty about the economic outlook as large segments of the economy were shut down, combined with concerns about markets’ ability to keep functioning in a remote environment, resulted in a strong desire for cash. In addition, the extreme volatility and its effect on risk metrics and margins meant that some normally profitable trades were no longer viable.

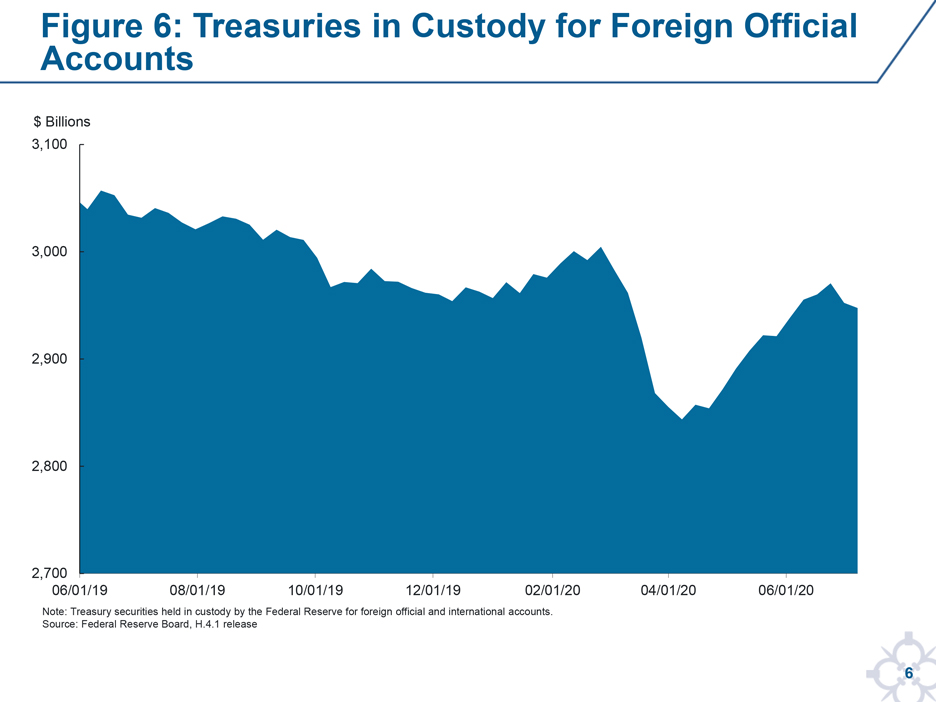

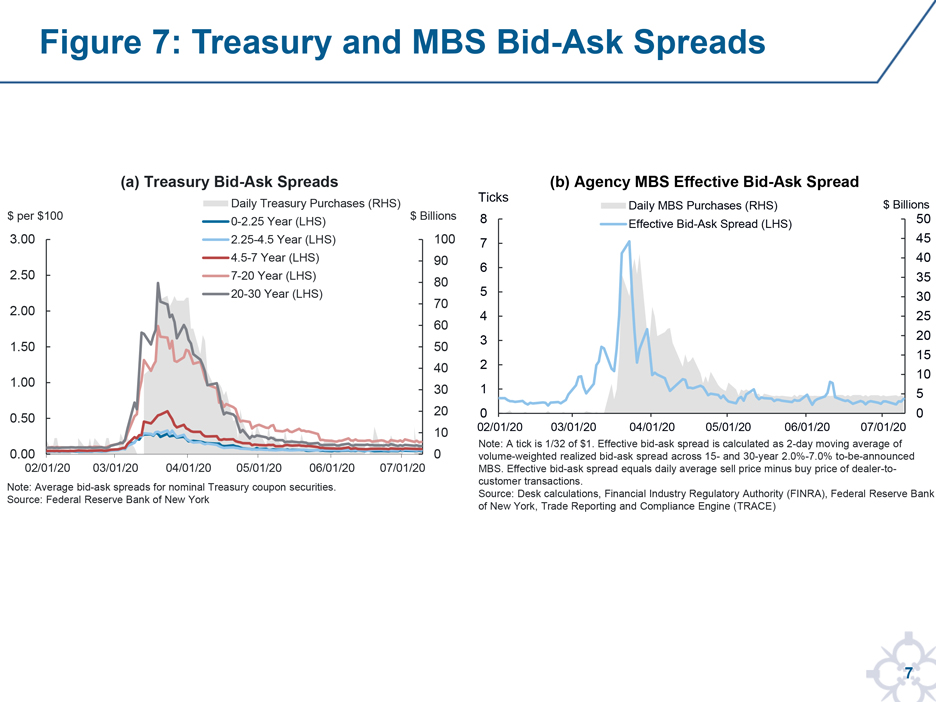

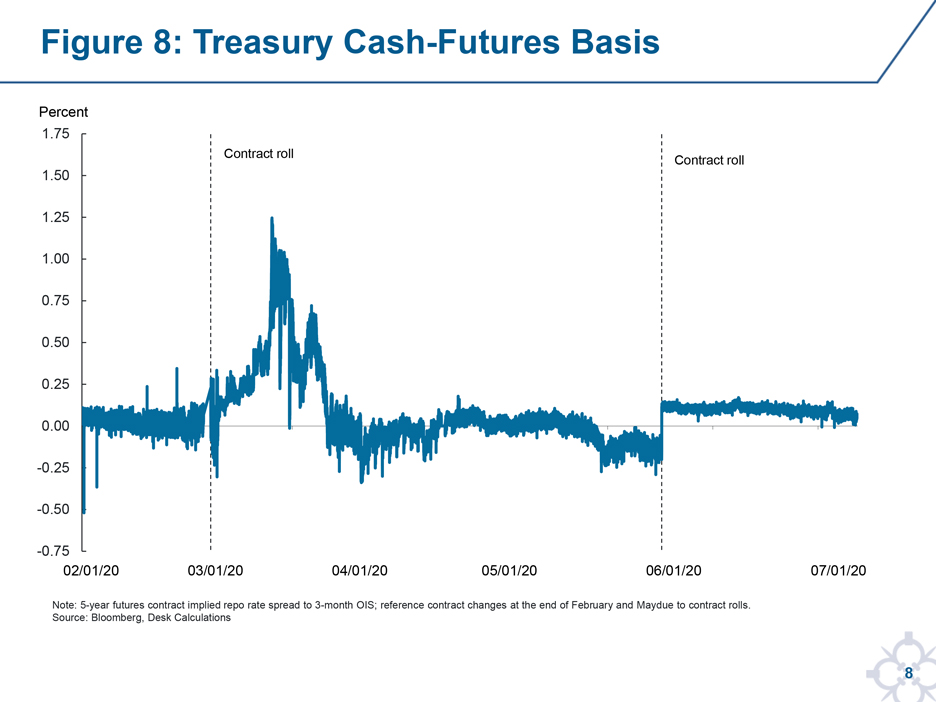

Investors and asset managers responded by rebalancing their portfolios, deleveraging, and acquiring the most liquid short-dated assets. In this environment, we saw a historically large flow of investor sales of Treasuries, as shown in Figure 5, as well as MBS. There were also notable sales by foreign reserve managers, whose Treasury securities held in custody at the Fed, shown in Figure 6, fell sharply during March. The flow strained the capacity of dealers and other liquidity providers to intermediate on normal terms. The challenges were particularly notable in off-the-run Treasuries, a sector where some dealers at times were reportedly reluctant to make markets at all. As a result, market functioning indicators were quite poor, as illustrated in Figure 7. Bid-ask spreads for Treasuries, in the left panel, and for agency MBS, in the right panel, both showed extraordinary increases. Relative value measures also widened notably, with prices appearing to diverge from fundamentals in some cases, as demonstrated by the Treasury cash-futures basis in Figure 8.9

At the FOMC’s direction, the Desk rapidly ramped up asset purchases to address these conditions. For the first few weeks, we had much to learn about how to maximize the effectiveness of purchases. We quickly adjusted operations based on our observations, and although it’s fair to say that at first we were mostly stabilizing market functioning, the purchases soon began to make meaningful improvements. As I’ll discuss in a moment, I think our flexibility itself played an important role in supporting market confidence.

I’ve been pleased to see that the functioning of Treasury and MBS markets has now rebounded notably. I was also pleased to see that, in the end, financial markets and infrastructures were able to continue operating even as the industry shifted, en masse, to working from home. Measures of market liquidity have uniformly improved and are now well below their worst points, though some remain more stressed than at the start of the year. In talking with our contacts, we hear that the lingering effects of the extraordinary volatility in March and the uncertain financial environment are limiting improvements in some liquidity metrics by reducing the appetite to take the risks associated with making markets. Relative value spreads have also narrowed substantially, though as with liquidity, some metrics remain higher than before the pandemic.

The Federal Reserve’s purchases have supported smooth market functioning through multiple channels. The purchases absorbed some of the flow of sales and helped restore two-way trading, which supports liquidity. In addition to absorbing a flow of securities, the purchases changed the stock of assets held by the private sector. Because the Desk accepts offers on securities with attractive prices, our operations can have the effect of buying undervalued securities and reducing price distortions.10

But these direct effects are not the only channels through which we think our purchases helped. The design of the purchase program also appeared to reduce market stress. I’d highlight two key aspects of the program in this regard: commitment and flexibility. The FOMC’s unlimited commitment to purchases “in the amounts needed” to support smooth market functioning was essential. Our market intelligence indicated that some investors had been selling not because they needed liquidity immediately, but because they wanted to take precautions against a further deterioration in market functioning. By providing confidence that the Treasury and MBS markets would remain liquid, the FOMC’s commitment to purchases reduced this motive for sales and helped calm the market.

Flexibility, as I noted earlier, has been another hallmark of our purchases that has helped to support confidence in smooth functioning of the Treasury and agency MBS markets. For most of the spring, we issued calendars for our purchases one week at a time, rather than our usual monthly calendars, and revised these plans even daily when necessary. As our indicators showed changes in market functioning, we adapted by adjusting the size of our purchases, the distribution of purchases across sectors, and even the settlement timing of our agency MBS operations.11 This flexibility has allowed us to maximize support for smooth market functioning. Once we saw improvements in market functioning, we began reducing the pace of our purchases starting in late March—but we did so gradually to reduce the chance of renewed disruptions, and we have remained watchful for conditions that would warrant an increase in purchases.

How Will We Sustain Smooth Market Functioning?

By the time of the FOMC’s June meeting, we had reduced the pace of purchases to the equivalent of around $80 billion per month in Treasuries and about $40 billion per month, net of reinvestments, in MBS.12 The FOMC directed the Desk in June to continue increasing SOMA holdings at least at this pace to sustain smooth market functioning, thereby fostering effective transmission of monetary policy to broader financial conditions.

Although market functioning has improved markedly since the period of extreme stress in mid-March, uncertainty about the course of the pandemic makes it prudent to protect against further shocks. There also are still sectors of the market where liquidity and pricing have not fully returned to pre-pandemic conditions. The continued work-from-home posture at many firms, and ongoing uncertainty in the outlook, appear to have made liquidity providers somewhat more cautious. Purchases over coming months will help mitigate risks of renewed stress and sustain continued smooth market functioning.

With the shift to a program focused on sustaining smooth market functioning, we are now announcing a monthly purchase amount and have lengthened our purchase schedules to semi-monthly periods for both Treasuries and MBS. These longer calendars provide greater foresight into our purchase plans, allowing dealers to prepare for this activity in the context of their customer flows. Importantly, though, we will remain vigilant for signs of deterioration in market functioning and flexible in adjusting our operations as needed. This strategy will allow us to safeguard the gains we’ve made and support the continued flow of credit to American families and businesses.

I’d emphasize in this regard that our assessment of market functioning is focused on indicators of market liquidity and efficient prices—not on the level of yields. It is certainly the case that the FOMC’s purchases have been absorbing duration and prepayment risk from the market. The total duration included in our Treasury purchases so far represents the equivalent of about $1 trillion in 10-year securities. Although term premiums do not appear to have come down significantly relative to just before the pandemic, our usual analysis indicates that our purchases have offset some upward pressure that could otherwise have occurred, for example as a result of the recent increases in Treasury debt issuance. I expect that the ongoing purchases will continue to absorb interest rate risk from the market, and that a wide range of factors other than our purchases will also continue to influence yields as our current purchases proceed.

Overall, I am confident that the full range of Federal Reserve programs, including the Treasury and MBS purchases, will mitigate the ongoing risks to market functioning and sustain the progress we have seen. The economic and financial shocks resulting from the pandemic have been truly extreme. The Federal Reserve’s commitment to smooth market functioning should provide continued confidence amid the ongoing public health and economic uncertainties.

Still, considering the crucial role of the Treasury and MBS markets in the financial system, and their growing size, it is important to ensure that these markets remain resilient to future shocks. What factors made these markets vulnerable to the abrupt deterioration in functioning that we saw in March? Could changes in regulations, data availability, or market infrastructure make market functioning more robust to future shocks? What role do funding markets play? These are challenging questions. They will require careful research and analysis, and they may not have simple answers. Still, the official and private sectors should be prepared to work together to assess them, and to do what it takes to ensure the continued strength and good functioning of these important markets.

Thank you.